Best Personal Loans For Fair Credit Of 2025

.eat-widget-container{border:1px solid #ededed;border-radius:.5rem;box-shadow:0 6px 9px rgba(0,0,0,.06);margin:20px 0;padding:16px}.eat-widget-container .eat-header{display:flex;font-family:EuclidCircularB,sans-serif;font-size:16px;font-weight:600;line-height:22px;padding-right:48px;word-break:break-word}.eat-widget-container .eat-header h2{border-style:none;margin:0;padding:0}.eat-widget-container .eat-header .eat-heading{color:#181716;font-weight:600;line-height:22px;margin:0 0 0 8px}.eat-widget-container .eat-header p.eat-heading{font-size:20px}@media (min-width:1025px){.eat-widget-container .eat-header p.eat-heading{font-size:24px}}.eat-widget-container .eat-header .eat-forbes-icon{flex-shrink:0;margin-top:2px}@media (min-width:768px){.eat-widget-container .eat-header .eat-forbes-icon{margin-top:1px}}.eat-widget-container .eat-wrapper{display:flex;flex-direction:column;padding-bottom:4px;padding-top:10px}.eat-widget-container .eat-wrapper h2{border-style:none}.eat-widget-container .eat-wrapper p{font-family:Georgia,serif;font-size:16px;line-height:26px}.eat-widget-container .eat-wrapper p:last-child{margin-bottom:0}@media (min-width:1024px){.eat-widget-container .eat-wrapper{flex-direction:row}.eat-widget-container .eat-wrapper.left-section-enabled .left-section,.eat-widget-container .eat-wrapper.right-section-enabled .right-section{width:100%}.eat-widget-container .eat-wrapper.right-section-enabled.left-section-enabled .left-section{width:60%}.eat-widget-container .eat-wrapper.left-section-enabled.right-section-enabled .right-section{padding-left:17px;width:40%}}.eat-widget-container .eat-wrapper ol{list-style-position:outside;list-style-type:decimal;margin-bottom:16px}.eat-widget-container .eat-wrapper ol:last-child{margin-bottom:0}.eat-widget-container .eat-wrapper ol li{font-size:14px;line-height:21px;margin-bottom:12px}.eat-widget-container .eat-wrapper ol li:last-child{margin-bottom:0}.eat-widget-container .eat-wrapper ul{margin:0 0 16px}.eat-widget-container .eat-wrapper ul:last-child{margin-bottom:0}.eat-widget-container .eat-wrapper ul li{font-family:EuclidCircularB,sans-serif;font-size:14px;line-height:21px;list-style-type:none;margin-bottom:12px;padding-left:27px;position:relative}.eat-widget-container .eat-wrapper ul li:last-child{margin-bottom:0}.eat-widget-container .eat-wrapper ul li:before{background:url(“data:image/svg+xml;charset=utf-8,%3Csvg width=’17’ height=’17’ fill=’none’ xmlns=’http://www.w3.org/2000/svg’%3E%3Cg clip-path=’url(%23a)’%3E%3Cpath d=’M15.583 7.852v.652a7.083 7.083 0 1 1-4.2-6.474m4.2.803L8.5 9.923 6.375 7.8′ stroke=’%237894D6′ stroke-width=’2′ stroke-linecap=’round’ stroke-linejoin=’round’/%3E%3C/g%3E%3Cdefs%3E%3CclipPath id=’a’%3E%3Cpath fill=’%23fff’ d=’M0 0h17v17H0z’/%3E%3C/clipPath%3E%3C/defs%3E%3C/svg%3E”) no-repeat;content:””;display:inline-block;height:20px;left:0;position:absolute;right:0;top:2px;width:20px}.eat-widget-container .eat-wrapper .left-section{order:2}@media (min-width:1024px){.eat-widget-container .eat-wrapper .left-section{order:0}}.eat-widget-container .eat-wrapper .right-section{flex-shrink:0;margin-bottom:16px;order:1;word-break:break-word}@media (min-width:1024px){.eat-widget-container .eat-wrapper .right-section{margin-bottom:0;order:0;padding-bottom:0}}.eat-widget-container .eat-wrapper a,.eat-widget-container .eat-wrapper b,.eat-widget-container .eat-wrapper em,.eat-widget-container .eat-wrapper i,.eat-widget-container .eat-wrapper span,.eat-widget-container .eat-wrapper strong{font-family:inherit;font-size:inherit;line-height:inherit}.eat-widget-container .eat-wrapper b,.eat-widget-container .eat-wrapper strong{font-weight:600}.eat-widget-container .eat-header-wrap{cursor:pointer;position:relative}.eat-widget-container .eat-header-wrap:after{background:url(“data:image/svg+xml;charset=utf-8,%3Csvg width=’20’ height=’20’ fill=’none’ xmlns=’http://www.w3.org/2000/svg’%3E%3Cpath fill-rule=’evenodd’ clip-rule=’evenodd’ d=’M15.838 0H4.162c-.527 0-.981 0-1.356.03-.395.033-.789.104-1.167.297A3 3 0 0 0 .327 1.638c-.193.378-.264.772-.296 1.167C0 3.18 0 3.635 0 4.161V15.84c0 .527 0 .981.03 1.356.033.395.104.789.297 1.167a3 3 0 0 0 1.311 1.311c.378.193.772.264 1.167.296.375.031.83.031 1.356.031H15.84c.527 0 .981 0 1.356-.03.395-.033.789-.104 1.167-.297a3 3 0 0 0 1.311-1.311c.193-.378.264-.772.296-1.167.031-.375.031-.83.031-1.356V4.16c0-.527 0-.981-.03-1.356-.033-.395-.104-.789-.297-1.167A3 3 0 0 0 18.362.327c-.378-.193-.772-.264-1.167-.296A17.9 17.9 0 0 0 15.838 0ZM10 5a1 1 0 0 1 1 1v3h3a1 1 0 1 1 0 2h-3v3a1 1 0 1 1-2 0v-3H6a1 1 0 1 1 0-2h3V6a1 1 0 0 1 1-1Z’ fill=’%2344549C’/%3E%3C/svg%3E”) no-repeat;content:””;display:inline-block;height:20px;position:absolute;right:0;top:10px;transform:translateY(-50%);transition:all .3s ease;width:20px}.eat-widget-container .eat-header-wrap.active:after{background:url(“data:image/svg+xml;charset=utf-8,%3Csvg width=’20’ height=’20’ fill=’none’ xmlns=’http://www.w3.org/2000/svg’%3E%3Cpath fill-rule=’evenodd’ clip-rule=’evenodd’ d=’M15.838 0H4.162c-.527 0-.981 0-1.356.03-.395.033-.789.104-1.167.297A3 3 0 0 0 .327 1.638c-.193.378-.264.772-.296 1.167C0 3.18 0 3.635 0 4.161V15.84c0 .527 0 .981.03 1.356.033.395.104.789.297 1.167a3 3 0 0 0 1.311 1.311c.378.193.772.264 1.167.296.375.031.83.031 1.356.031H15.84c.527 0 .981 0 1.356-.03.395-.033.789-.104 1.167-.297a3 3 0 0 0 1.311-1.311c.193-.378.264-.772.296-1.167.031-.375.031-.83.031-1.356V4.16c0-.527 0-.981-.03-1.356-.033-.395-.104-.789-.297-1.167A3 3 0 0 0 18.362.327c-.378-.193-.772-.264-1.167-.296A17.9 17.9 0 0 0 15.838 0ZM6 9a1 1 0 0 0 0 2h8a1 1 0 1 0 0-2H6Z’ fill=’%2344549C’/%3E%3C/svg%3E”) no-repeat}.edit-eat-widget{margin:0 0 10px}@media (min-width:768px){.page-template .eat-widget-container:has(.eat-header-wrap.active),.post-template .eat-widget-container:has(.eat-header-wrap.active),.post-template-default .eat-widget-container:has(.eat-header-wrap.active){padding-bottom:24px}}.page-template .eat-widget-container .eat-header-wrap:after,.post-template .eat-widget-container .eat-header-wrap:after,.post-template-default .eat-widget-container .eat-header-wrap:after{background:url(“data:image/svg+xml;base64,PHN2ZyB3aWR0aD0iMjAiIGhlaWdodD0iMjAiIGZpbGw9Im5vbmUiIHhtbG5zPSJodHRwOi8vd3d3LnczLm9yZy8yMDAwL3N2ZyI+PHBhdGggZmlsbC1ydWxlPSJldmVub2RkIiBjbGlwLXJ1bGU9ImV2ZW5vZGQiIGQ9Ik0xNS44MzggMEg0LjE2MmMtLjUyNyAwLS45ODEgMC0xLjM1Ni4wMy0uMzk1LjAzMy0uNzg5LjEwNC0xLjE2Ny4yOTdBMyAzIDAgMCAwIC4zMjcgMS42MzhjLS4xOTMuMzc4LS4yNjQuNzcyLS4yOTYgMS4xNjdDMCAzLjE4IDAgMy42MzUgMCA0LjE2MVYxNS44NGMwIC41MjcgMCAuOTgxLjAzIDEuMzU2LjAzMy4zOTUuMTA0Ljc4OS4yOTcgMS4xNjdhMyAzIDAgMCAwIDEuMzExIDEuMzExYy4zNzguMTkzLjc3Mi4yNjQgMS4xNjcuMjk2LjM3NS4wMzEuODMuMDMxIDEuMzU2LjAzMUgxNS44NGMuNTI3IDAgLjk4MSAwIDEuMzU2LS4wMy4zOTUtLjAzMy43ODktLjEwNCAxLjE2Ny0uMjk3YTMgMyAwIDAgMCAxLjMxMS0xLjMxMWMuMTkzLS4zNzguMjY0LS43NzIuMjk2LTEuMTY3LjAzMS0uMzc1LjAzMS0uODMuMDMxLTEuMzU2VjQuMTZjMC0uNTI3IDAtLjk4MS0uMDMtMS4zNTYtLjAzMy0uMzk1LS4xMDQtLjc4OS0uMjk3LTEuMTY3YTMgMyAwIDAgMC0xLjMxMi0xLjMxYy0uMzc4LS4xOTMtLjc3Mi0uMjY0LTEuMTY3LS4yOTZBMTcuOSAxNy45IDAgMCAwIDE1LjgzOCAwWk0xMCA1YTEgMSAwIDAgMSAxIDF2M2gzYTEgMSAwIDEgMSAwIDJoLTN2M2ExIDEgMCAwIDEtMiAwdi0zSDZhMSAxIDAgMCAxIDAtMmgzVjZhMSAxIDAgMCAxIDEtMVoiIGZpbGw9IiMwMDdBQzgiLz48L3N2Zz4=”) no-repeat}.page-template .eat-widget-container .eat-header-wrap.active:after,.post-template .eat-widget-container .eat-header-wrap.active:after,.post-template-default .eat-widget-container .eat-header-wrap.active:after{background:url(“data:image/svg+xml;base64,PHN2ZyB3aWR0aD0iMjAiIGhlaWdodD0iMjAiIGZpbGw9Im5vbmUiIHhtbG5zPSJodHRwOi8vd3d3LnczLm9yZy8yMDAwL3N2ZyI+PHBhdGggZmlsbC1ydWxlPSJldmVub2RkIiBjbGlwLXJ1bGU9ImV2ZW5vZGQiIGQ9Ik0xNS44MzguNUg0LjE2MmMtLjUyNyAwLS45ODEgMC0xLjM1Ni4wMy0uMzk1LjAzMi0uNzg5LjEwMy0xLjE2Ny4yOTZBMyAzIDAgMCAwIC4zMjcgMi4xMzdjLS4xOTMuMzc4LS4yNjQuNzcyLS4yOTYgMS4xNjdDMCAzLjY4IDAgNC4xMzQgMCA0LjY2djExLjY4YzAgLjUyNiAwIC45OC4wMyAxLjM1NS4wMzMuMzk1LjEwNC43OS4yOTcgMS4xNjdhMyAzIDAgMCAwIDEuMzExIDEuMzExYy4zNzguMTkzLjc3Mi4yNjQgMS4xNjcuMjk2LjM3NS4wMzEuODMuMDMxIDEuMzU2LjAzMUgxNS44NGMuNTI3IDAgLjk4MSAwIDEuMzU2LS4wMy4zOTUtLjAzMy43ODktLjEwNCAxLjE2Ny0uMjk3YTMgMyAwIDAgMCAxLjMxMS0xLjMxYy4xOTMtLjM3OS4yNjQtLjc3My4yOTYtMS4xNjguMDMxLS4zNzUuMDMxLS44My4wMzEtMS4zNTZWNC42NmMwLS41MjcgMC0uOTgtLjAzLTEuMzU2LS4wMzMtLjM5NS0uMTA0LS43ODktLjI5Ny0xLjE2N2EzIDMgMCAwIDAtMS4zMTItMS4zMUMxNy45ODQuNjMzIDE3LjU5LjU2MiAxNy4xOTUuNTNBMTcuOSAxNy45IDAgMCAwIDE1LjgzOC41Wk0xMCA5LjQ5OGwuNS4wMDFIMTRhMSAxIDAgMSAxIDAgMmgtNGwtLjUtLjAwMUg2YTEgMSAwIDAgMSAwLTJoM2wuMDIzLjAwMUg5LjVMMTAgOS41WiIgZmlsbD0iIzAwN0FDOCIvPjwvc3ZnPg==”) no-repeat}.page-template .eat-widget-container .eat-header,.post-template .eat-widget-container .eat-header,.post-template-default .eat-widget-container .eat-header{font-family:Work Sans,sans-serif}.page-template .eat-widget-container .eat-header .eat-forbes-icon,.post-template .eat-widget-container .eat-header .eat-forbes-icon,.post-template-default .eat-widget-container .eat-header .eat-forbes-icon{margin-top:-1px}@media (min-width:768px){.page-template .eat-widget-container .eat-header .eat-forbes-icon,.post-template .eat-widget-container .eat-header .eat-forbes-icon,.post-template-default .eat-widget-container .eat-header .eat-forbes-icon{margin-top:-1px}}.page-template .eat-widget-container .eat-header .eat-heading,.post-template .eat-widget-container .eat-header .eat-heading,.post-template-default .eat-widget-container .eat-header .eat-heading{color:#333}.page-template .eat-widget-container .eat-wrapper,.post-template .eat-widget-container .eat-wrapper,.post-template-default .eat-widget-container .eat-wrapper{padding-bottom:0}.page-template .eat-widget-container .eat-wrapper ul li,.post-template .eat-widget-container .eat-wrapper ul li,.post-template-default .eat-widget-container .eat-wrapper ul li{font-family:Work Sans,sans-serif}.page-template .eat-widget-container .eat-wrapper ul li:before,.post-template .eat-widget-container .eat-wrapper ul li:before,.post-template-default .eat-widget-container .eat-wrapper ul li:before{background:url(“data:image/svg+xml;base64,PHN2ZyB3aWR0aD0iMTgiIGhlaWdodD0iMTgiIGZpbGw9Im5vbmUiIHhtbG5zPSJodHRwOi8vd3d3LnczLm9yZy8yMDAwL3N2ZyI+PHBhdGggZD0iTTEzLjI3NyA3LjI2NWEuNzM1LjczNSAwIDEgMC0xLjA0LTEuMDM5bC0zLjk4OCAzLjk5LTIuNDg2LTIuNDg3YS43MzUuNzM1IDAgMSAwLTEuMDQgMS4wNGwzLjAwNiAzLjAwNWEuNzM1LjczNSAwIDAgMCAxLjA0IDBsNC41MDgtNC41MDlaIiBmaWxsPSIjMDA3QUM4Ii8+PHBhdGggZmlsbC1ydWxlPSJldmVub2RkIiBjbGlwLXJ1bGU9ImV2ZW5vZGQiIGQ9Ik05IDBhOSA5IDAgMSAwIDAgMThBOSA5IDAgMCAwIDkgMFpNMS40NyA5YTcuNTMgNy41MyAwIDEgMSAxNS4wNiAwQTcuNTMgNy41MyAwIDAgMSAxLjQ3IDlaIiBmaWxsPSIjMDA3QUM4Ii8+PC9zdmc+”) no-repeat}

Best Personal Loans for Fair Credit of 2025

Best for a Variety of Loan Options

LendingPoint

Minimum Credit Score

600

APR range

7.99% to 35.99%

with autopay

Loan amounts

$1,000 to $36,500

600

7.99% to 35.99%

with autopay

$1,000 to $36,500

Fair-credit borrowers can access a wide range of loan amounts and terms through LendingPoint.

Why We Like It

LendingPoint offers various loan options with loan amounts from $1,000 to $36,500 and repayment terms from 24 to 72 months—or two to six years.

What We Don’t Like

Borrowers pay origination fees up to 10% of their loan amount.

Who It’s Best For

LendingPoint is best for fair-credit borrowers who need a personal loan between $1,000 to $36,500.

- Quick funding

- Low credit score requirements

- No prepayment penalty

- Origination fee up to 10%

- Co-signers or joint loans not permitted

- Not available in Nevada and West Virginia

Eligibility:

- Minimum credit score. 600

- Minimum annual income. $35,000

- Co-signers. Not permitted

Customer service

After testing and evaluating LendingPoint’s customer service, we found it to be one of the most helpful and transparent lenders on our list after waiting only 46 seconds to be connected to a representative. The customer service representative we spoke with shared an in-depth perspective of their loan offers, including information about loan amounts, eligibility requirements, how interest rates are determined and prequalification.

LendingPoint’s team also disclosed late fees but didn’t confirm origination fees. While customer service didn’t share this information wasn’t, the lender discloses a fee of up to 10% on its website. LendingPoint was also one of few lenders that shared how they report payments to credit bureaus, which it typically does at the start of the month.

Best for Small Amounts

OneMain Financial

Minimum Credit Score

OneMain Financial does not disclose this information

APR range

18.00% to 35.99%

Loan amounts

$1,500 to $20,000

OneMain Financial does not disclose this information

18.00% to 35.99%

$1,500 to $20,000

OneMain Financial offers small personal loans starting at $1,500 to $20,000.

Why We Like It

OneMain Financial funds its loans within an hour if you receive your funds via a debit card, but one to two banking days if you choose direct deposit.

What We Don’t Like

OneMain Financial charges either an origination fee that’s 1% to 10% of your loan amount or a flat fee from $25 to $500.

Who It’s Best For

OneMain Financial is best for borrowers who need small loans with fast funding times.

- Designed for borrowers with low credit scores

- Offers secured loan options

- Evaluates entire credit and income history instead of credit score

- Limits only up to $20,000

- Can’t be used for business purposes

- Charges high APRs

Eligibility:

- Minimum credit score required. No minimum credit score requirement

- Minimum annual income. No minimum income requirement

- Co-borrowers. Not permitted

- Co-signers. Permitted

Best for Long Terms

Upgrade

Minimum Credit Score

620

APR range

7.99% to 35.99%

Loan amounts

$1,000 to $50,000

620

7.99% to 35.99%

$1,000 to $50,000

Upgrade’s flexible credit score requirements and long loan terms make it a top choice for fair-credit borrowers.

Why We Like It

Upgrade allows for a minimum credit score of 620 and offers loan terms of two to seven years. It also provides a variety of interest-rate discounts.

What We Don’t Like

Borrowers need to be aware of Upgrade’s high maximum annual percentage rate (APR) of 35.99%. Upgrade also charges origination fees between 1.85% and 9.99% of your loan amount. Both of these factors can make its loans costly.

Who It’s Best For

Upgrade personal loans are best for borrowers with limited credit looking for long-term loans.

- Fair credit accepted

- Rate discounts for using autopay and for using loans to pay off existing debt

- Free credit health monitoring

- Origination fees

- Potentially high interest rates

Eligibility

- Minimum credit score: 620620

- Co-applicants: Permitted

- Direct pays third-party creditors: Yes

Customer service

We called Upgrade to gauge the responsiveness of its customer service team and found it to be one of the most responsive lenders on our list. While we waited just over one minute for their team to answer our call—which is not the fastest time—they were transparent and knowledgeable about Upgrade’s loans.

We received information on loan amounts, required documentation, interest rate ranges, approval speed, fees and various perks, like hardship programs and autopay discounts. The representative also confirmed that they report payments to credit bureaus.

Disclosure

Personal loans made through Upgrade feature Annual Percentage Rates (APRs) of 7.99%-35.99%. All personal loans have a 1.85% to 9.99% origination fee, which is deducted from the loan proceeds. Lowest rates require Autopay and paying off a portion of existing debt directly. Loans feature repayment terms of 24 to 84 months. For example, if you receive a $10,000 loan with a 36-month term and a 17.59% APR (which includes a 13.94% yearly interest rate and a 5% one-time origination fee), you would receive $9,500 in your account and would have a required monthly payment of $341.48. Over the life of the loan, your payments would total $12,293.46. The APR on your loan may be higher or lower and your loan offers may not have multiple term lengths available. Actual rate depends on credit score, credit usage history, loan term, and other factors. Late payments or subsequent charges and fees may increase the cost of your fixed-rate loan. There is no fee or penalty for repaying a loan early. Personal loans issued by Upgrade’s bank partners. Information on Upgrade’s bank partners can be found at https://www.upgrade.com/bank-partners/.

Best for Joint Loans

LendingClub

Minimum Credit Score

600

APR range

7.90% to 35.99%

Loan amounts

$1,000 to $40,000

600

7.90% to 35.99%

$1,000 to $40,000

LendingClub is a full-service online lender that offers personal loans from $1,000 to $40,000. Repayment terms range from two to five years.

Why We Like It

LendingClub has a low barrier to entry with its flexible credit score requirements. It also allows for co-borrowers or joint loans, which can help improve approval odds.

What We Don’t Like

LendingClub charges origination fees of 0% to 8% of your loan amount.

Who It’s Best For

LendingClub personal loans are best for borrowers who want to apply with a co-borrower to improve their approval odds.

- Low credit score requirement

- Rate discount for using funds to pay off debt

- Accepts co-applicants

- Origination fees

- High potential rates

Eligibility

- Minimum credit score: 600

- Co-applicants: Permitted

- Direct pays third-party creditors: Yes

Customer service

We tested LendingClub’s customer service to assess how helpful it is for prospective borrowers and found the representative could provide only surface-level answers. For example, after waiting just over one minute to connect with a rep, they confirmed you can set up autopay but did not confirm if any autopay discounts are available. In another case, they mentioned LendingClub charges an origination fee but didn’t disclose anything further like the amount.

However, this does not mean they were not responsive or able to provide helpful information. We connected with a rep in just over one minute. Through our evaluation, we gathered key information, including loan amounts, required documentation such as W-2s and bank statements, loan assistance options and funding turnaround times.

Best for Low Interest Rates

LightStream

Minimum Credit Score

660

APR range

6.49% to 25.29%

with autopay

Loan amounts

$5,000 to $100,000

660

6.49% to 25.29%

with autopay

$5,000 to $100,000

LightStream offers personal loans with competitive interest rates and quick turnaround times.

Why We Like It

LightStream’s personal loans advertise competitive interest rates between 6.49% to 25.29%. It can also fund loans the same day you submit your application.

What We Don’t Like

Although LightStream has a minimum credit score requirement of 660, fair-credit borrowers may have trouble qualifying.

Who It’s Best For

LightStream’s personal loans are best for borrowers with fair to good credit who can qualify for low interest rates.

- No origination fee

- Rate discounts for using autopay

- High loan amounts and extended terms

- No feature to direct pay creditors

- No option to prequalify without a hard inquiry

Eligibility

- Minimum credit score: 660

- Co-applicants: Permitted

- Direct pays third-party creditors: No

Customer service

We tried to call LightStream to test the quality of its customer service, but they don’t provide a customer service number. If you want to reach their customer service team, you must contact them via email. Its email support is available Monday through Friday, 9:30 am to 7 pm and Saturday, 12 to 4 pm ET.

Best for Large Amounts

SoFi®

Minimum Credit Score

650

APR range

8.99% to 35.49%

with all discounts

Loan amounts

$5,000 to $100,000

650

8.99% to 35.49%

with all discounts

$5,000 to $100,000

SoFi is a full-service online lender that offers a range of banking services and personal loans from $5,000 to $100,000.

Why We Like It

SoFi boasts large loan amounts and repayment terms from two to seven years. While it charges no loan fees, you can pay an optional origination fee for a lower interest rate.

What We Don’t Like

SoFi has a fairly high credit score requirement of 650, making its personal loans out of reach for some borrowers.

Who It’s Best For

SoFi personal loans are best for fair-credit borrowers who can meet the minimum credit score requirement and need large loan amounts.

- No origination fees or late fees

- Rate discounts for using autopay

- Direct pay to third-party creditors

- Strong credit may be necessary

- Rates higher than other lenders

Eligibility

- Minimum credit score: 650

- Co-applicants: Permitted

- Direct pays third-party creditors: Yes

Customer service

We evaluated SoFi’s customer service experience by calling its team directly. During our assessment, we found that its wait times were some of the longest—one minute and 41 seconds. Once we connected with customer service, its team was able to answer each of our questions effectively.

They disclosed loan amounts, available interest rates, required documents and loan approval times. They also shared information about prequalification and potential fees.

Best for Customer Experience

Avant

Minimum Credit Score

550

APR range

9.95% to 35.99%

Loan amounts

$2,000 to $35,000

550

9.95% to 35.99%

$2,000 to $35,000

Fair-credit borrowers who value a quality customer experience should look no further than Avant.

Why We Like It

Avant offers borrowers solid customer service options, including availability seven days a week, a mobile app and an online application. Its Trustpilot ratings are also high.

What We Don’t Like

Avant charges an administration fee of up to 9.99% and late payment fees of $25.

Who It’s Best For

Avant’s personal loans are best for fair-credit borrowers who value customer satisfaction and need a personal loan from $2,000 to $35,000.

- Secured and unsecured loan options available

- Low credit score requirement of 550

- Loan terms available up to 60 months

- Charges an upfront administrative fee

- High minimum APR

- Co-signers and co-applicants not allowed

Eligibility

- Minimum credit score. 550

- Minimum income. Does not disclose

- Co-borrowers. Not permitted

- Co-signers. Not permitted

Best for an Alternative Qualification Process

Upstart

Minimum Credit Score

620

APR range

6.70% to 35.99%

Loan amounts

$1,000 to $50,000

620

6.70% to 35.99%

$1,000 to $50,000

Upstart uses AI to speed up its evaluation process, which considers alternative qualification factors. This allows Upstart to offer more flexible credit requirements.

Why We Like It

While Upstart’s minimum credit score requirement is 620, it also considers borrowers without sufficient credit history.

What We Don’t Like

Upstart charges origination fees up to up to 12% of your loan amount. What’s more, Upstart repayment terms are limited to three- or five-years.

Who It’s Best For

Upstart personal loans are best for prospective borrowers with limited credit histories.

- Accessible to borrowers with no credit history

- Prequalification with a soft credit check

- Ability to choose a custom payment date

- Charges an origination fee up to 12% of the loan amount

- No co-signer option

- Only offers three- or five-years terms

Eligibility

- Minimum credit score. 620

- Minimum income. No minimum but must have a source of income

- Co-signers. Not permitted

- Co-borrowers. Not permitted

Customer service

We tested Upstart’s customer service quality to evaluate its helpfulness. Through our research, we found Upstart’s team was one of the fastest to answer, as we waited only 39 seconds. However, once connected, the representative was vague. While they disclosed general loan details like loan amounts, fees and interest rate ranges, they were unclear about documentation requirements and approval times.

Summary: Best Personal Loans for Fair Credit of 2025

| COMPANY | FORBES ADVISOR RATING | MINIMUM CREDIT SCORE | APR RANGE | LOAN AMOUNTS | LEARN MORE |

|---|---|---|---|---|---|

| 600 | 7.99% to 35.99% | $1,000 to $36,500 | Via MoneyLion’s Website | |

| | OneMain Financial does not disclose this information | 18.00% to 35.99% | $1,500 to $20,000 | Via Credible.com’s Website | |

| 620 | 7.99% to 35.99% | $1,000 to $50,000 | Via Credible.com’s Website | |

| | 600 | 7.90% to 35.99% | $1,000 to $40,000 | Via Credible.com’s Website | |

| 660 | 6.49% to 25.29% | $5,000 to $100,000 | Via Credible.com’s Website | |

| | 650 | 8.99% to 35.49% with all discounts | $5,000 to $100,000 | Via Credible.com’s Website | |

| | 550 | 9.95% to 35.99% | $2,000 to $35,000 | Via Credible.com’s Website | |

| | 620 | 6.70% to 35.99% | $1,000 to $50,000 | Via Credible.com’s Website |

How To Compare Personal Loans for Fair Credit

Most lenders disclose the information you need to compare your loan options on their website, including loan terms, interest rates, fees and, in some cases, even qualification requirements. However, prequalifying for loan offers can give you a better idea of the rates and terms lenders may offer you without impacting your credit.

Once you’re ready to compare loan offers, consider these loan features:

- Annual percentage rate (APR). APR is the total cost of borrowing money, including interest and fees. Comparing your APR offers can be the most efficient way to find the lowest-cost option. Other loan features are also essential to consider.

- Loan terms. Each lender offers different loan terms or the time you have to repay a loan. The loan terms influence your monthly payment. Before you accept a loan, be sure you can afford to repay the loan on time.

- Loan amounts. If you have fair credit and need a large loan, some lenders may not offer you the full amount. If this is the case, you can narrow down your options depending on where you can get a sufficient loan amount.

- Qualification requirements. If you’re applying for personal loans with fair credit, you likely won’t be able to qualify with just any lender. Before applying, be sure you meet the lender’s minimum qualification requirements.

- Fees and penalties. Fees and penalties, including origination fees, prepayment penalties and late payment fees, vary between lenders. If, for instance, you plan to repay your loan early, look for lenders that charge no prepayment penalties.

- Perks. Some lenders offer perks, such as discounts for automatic payments or payment deferral if you need forbearance. Consider whether you would use these features when comparing your loan options.

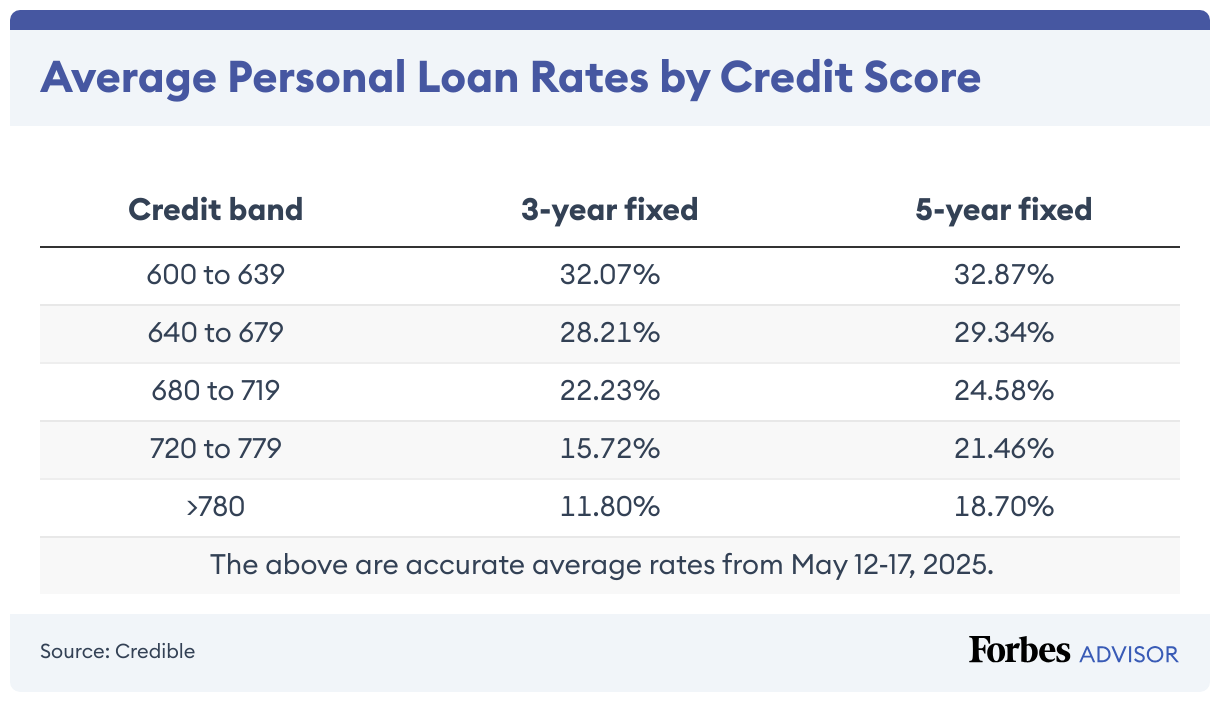

How Does Fair Credit Impact Interest Rates?

Most lenders use your score to help determine your ability to manage debt. If you have fair credit (580 to 669 on the FICO scale), it can be challenging to qualify for a lender’s lowest advertised interest rates.

Nonetheless, your credit score is just one part of a loan application. Maintaining a high income or a small amount of debt compared to your income—represented as your debt-to-income (DTI) ratio—can help you qualify for lower rates.

If your application is denied, you’ll receive an adverse action letter explaining the rejection. It can be worthwhile to address the issues noted in the letter before applying for other loans, which may also help you receive lower interest rates.

Average Personal Loan Rates By Credit Score

How To Qualify for the Lowest Possible Rates

Fair credit can make it hard to get the lowest advertised rates, but there are steps you can take to receive lower rates, including:

- Improve your credit. You can quickly improve your credit by paying down debts to reduce your credit utilization rate, requesting higher credit limits and correcting any errors on your credit report. If you increase your credit limit, be sure not to use it or your credit utilization rate will increase, which may harm your credit score.

- Lower your DTI. Paying down debt (or increasing your income) can reduce your DTI. Lenders use your DTI to determine your ability to repay a loan.

- Shop around. Considering a wide range of lenders, including credit unions and online lenders, can help you find the lowest interest rates. Compare prequalification offers to determine which lender is best.

Alternatives to a Fair Credit Loan

If your credit score is sufficient, there are alternatives you can consider, including:

- Secured personal loans. With a secured personal loan, borrowers offer up collateral to back the cost of the loan. Secured loans can be easier to qualify for because if you fail to repay the loan, the lender can take possession of your collateral.

- Home equity financing. Home equity loans or lines of credit use the equity you’ve built in your home to get funding. These loans may come with lower interest rates than personal loans. However, because your home secures the loan, the lender can repossess your home if you fail to repay.

- Credit cards. If you need to cover a short-term financial emergency, credit cards can be an effective tool if you have a plan to repay your debt. Keep in mind, it can be easy to overspend on a credit card, and high APRs and fees can make carrying a balance expensive.

- Cash advance apps. Cash advance apps offer short-term loans—typically two weeks—in small amounts. These loans can be a good option to cover a small financial need, but missing payments can lead to late fees and other penalties.

- Savings. Saving to cover your expenses rather than taking out a loan will let you avoid interest and the burden of repaying a loan for years to come.

- Friends and family. If you have friends or family willing to lend you money, this can be a good option to cover your financial needs. Before accepting any funding, consider writing a promissory note so both parties agree on the loan terms.

Methodology

We reviewed 44 popular lenders based on 20 data points in the categories of customer sentiment index, loan details, loan costs, eligibility and accessibility and the application process. We chose the best lenders based on the weighting assigned to each category:

- Customer sentiment index. 40%

- Eligibility and accessibility. 25%

- Loan details. 15%

- Loan costs. 13%

- Application process. 7%

We also considered several characteristics within each major category, including available loan amounts, repayment terms, APR ranges and applicable fees. We also looked at minimum credit score requirements, whether each lender accepts co-signers or joint applications and the geographic availability of the lender. Finally, we evaluated each provider’s customer support tools, borrower perks and features that simplify the borrowing process—such as prequalification options and mobile apps.

Where appropriate, we awarded partial points depending on how well a lender met each criterion.

To learn more about how Forbes Advisor rates lenders, and our editorial process, check out our Personal Loans Rating Methodology.

Next Up In Personal Loans